Preparing Utility Cost Data for Refinancing or Disposition

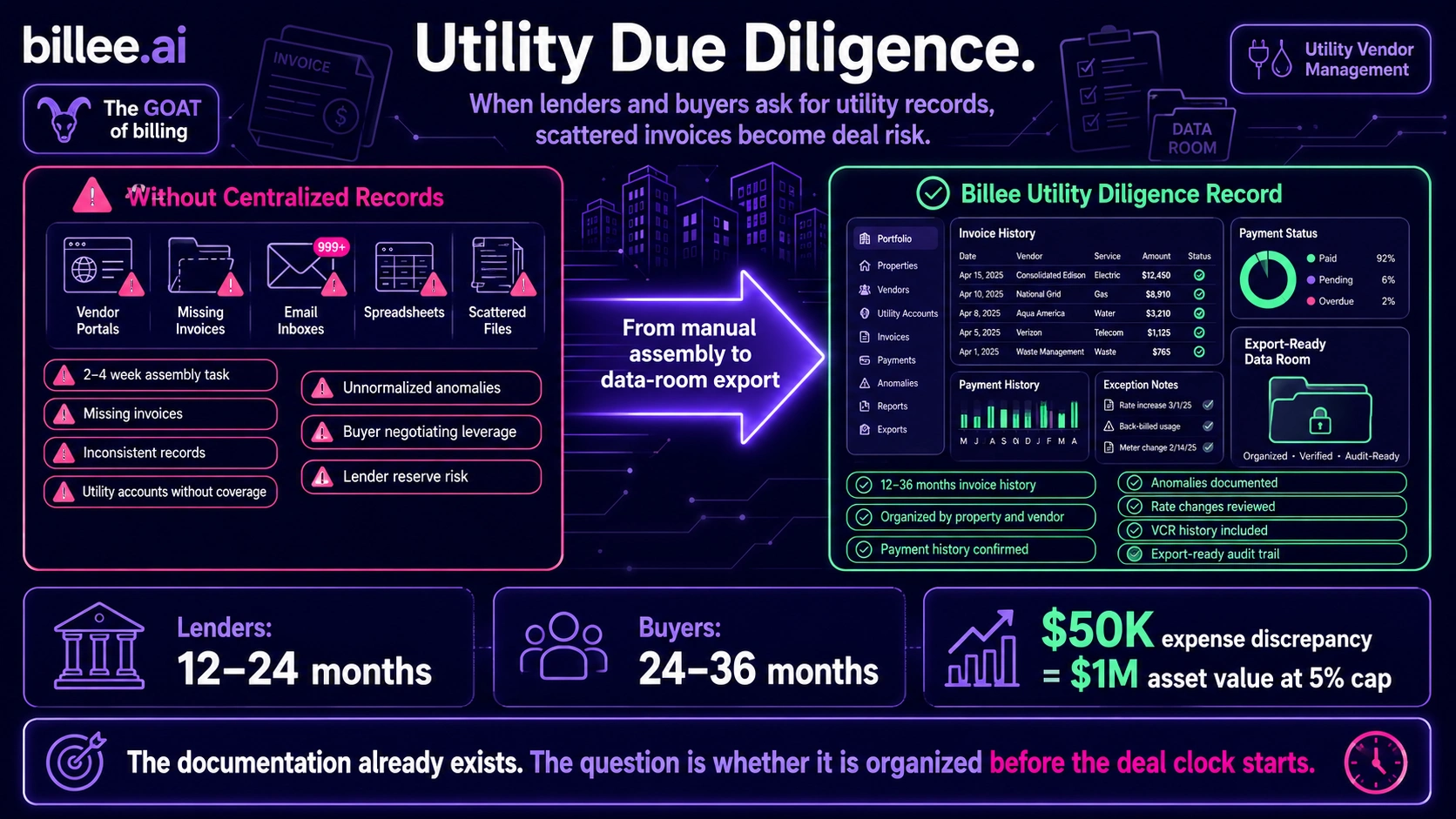

When a lender or buyer requests utility expense documentation during due diligence, operators without centralized records face a two-to-four-week assembly task that often produces an incomplete result. Gaps in utility payment history give buyers a negotiating lever and can trigger lender-required reserves, both of which affect deal terms. The documentation required (12–36 months of invoice history organized by property and vendor, with consumption anomalies identified and normalized) already exists in any operator's AP records; the question is whether it is organized, complete, and accessible. Billee's Utility Vendor Management product maintains that record as a byproduct of normal AP processing, so diligence requests are answered in hours rather than weeks.

Key Takeaways

Lenders typically require 12–24 months of utility payment history at refinancing; buyers in an acquisition often go to 24–36 months. The scope depends on transaction type and financing structure.

Documentation gaps (missing invoices, accounts without coverage, inconsistent records across properties) give buyers a negotiating lever. Buyers use gaps to justify price adjustments or escrow holds, regardless of whether the gaps reflect actual billing problems.

The trailing 12-month utility expense figure almost always requires normalization before it can represent the true forward run rate. Consumption anomalies, one-time events, and mid-year rate increases each distort the raw figure in different directions.

A utility expense record that shows consistent, well-managed billing (clean payment history, organized by property and vendor) is a positive disclosure that supports stated NOI and reinforces the cap-rate valuation.

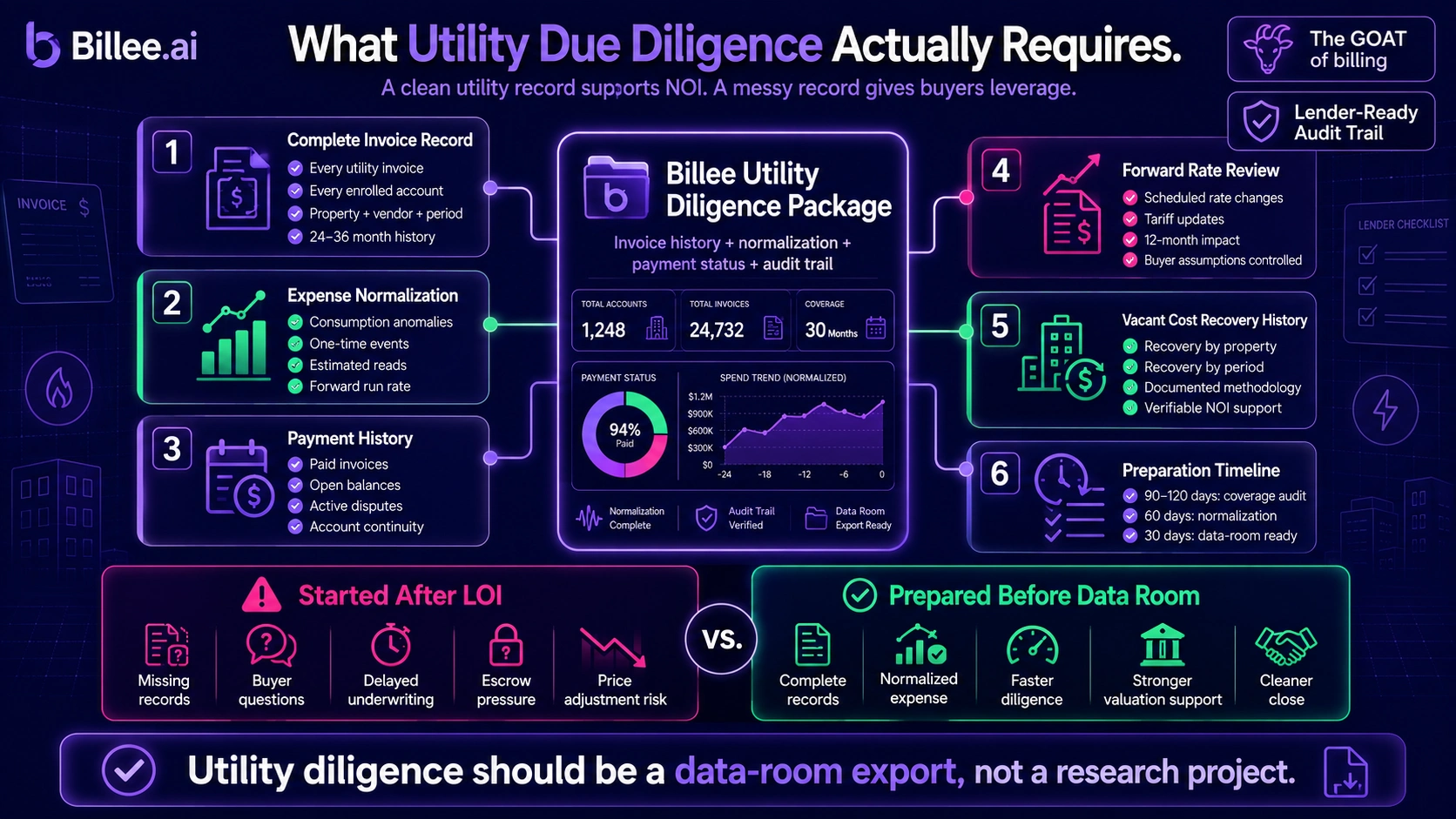

The time to start assembling utility diligence documentation is 90–120 days before a target close, not when the data room opens. Assembly started after an LOI becomes a closing-timeline risk.

Billee's invoice history is organized by property, vendor, and billing period from enrollment forward; the diligence package is a data-room export, not a research project.

Why Utility Expense Documentation Matters in a Transaction

Utility expense is one of the largest operating lines in a multifamily property and a direct component of NOI. At a 5% cap rate, a $50,000 discrepancy in the utility expense run rate represents $1 million in asset value. Both lenders and buyers scrutinize utility expense closely because it is variable, vendor-managed, and historically a source of billing errors and management gaps.

Lenders underwriting a refinancing use the operating expense schedule to verify debt service coverage. If the utility expense history is inconsistent or incomplete, underwriting stalls. Buyers verifying a seller's stated NOI want to confirm that utility expense is real, current, and representative of forward operations.

A clean, complete, normalized utility expense record supports the valuation. An inconsistent one creates questions that cost time and negotiating position to resolve.

What Lenders Request at Refinancing

Standard multifamily loan underwriting, including Fannie Mae and Freddie Mac programs, requires trailing income and expense documentation as part of operating expense verification. For utility expense, lenders typically want 12–24 months of invoice records by property, confirmation of no unpaid balances with active utility vendors, and no unresolved billing disputes on the account.

What creates problems in the lender's review: gaps in account coverage (utility accounts not tracked in the AP system), invoices that were paid but not retained, and properties where utility accounts changed mid-period and the history was not consolidated. Any of these can trigger a request for additional documentation, which adds weeks to the underwriting timeline. Persistent gaps can result in a lender-required utility expense reserve that effectively increases the cost of the financing before the loan even closes.

What Buyers Request at Disposition

Buyers typically go deeper than lenders and with a different objective. Where a lender is verifying that the expense is real and payments are current, a buyer is trying to determine whether the trailing expense represents the forward run rate. That requires understanding the trend over 24–36 months, identifying and normalizing anomalies, and assessing whether known rate changes will alter the forward expense materially.

Buyers will identify anomalies whether the seller discloses them or not. An undisclosed Q2 water spike discovered in the invoice records is a negotiating point: the buyer assumes it reflects ongoing risk rather than a one-time event that has been resolved. Sellers who disclose anomalies with supporting documentation and a normalized figure control the narrative; sellers who don't give buyers a lever.

Vacant Cost Recovery history is also a positive disclosure at disposition. An operator who can document a VCR program with a multi-year recovery track record is demonstrating active management of a line that most operators leave untracked. That documentation supports NOI and differentiates the asset in a competitive process.

Preparing the Utility Diligence Package

The preparation task has six components. Each requires different data and different lead time. Operators who start 90 days before close arrive at the data room with a complete package. Operators who start when the LOI arrives are still assembling records while the clock runs.

Assembling the Invoice Record

The foundation of the diligence package is a complete invoice record: every utility invoice for every enrolled account, organized by property, vendor, and billing period, for the trailing 24–36 months. For most operators, this data is distributed across individual vendor portals (each utility company has its own login), the property management system (payment records, but rarely invoice copies), email inboxes at the property level, and local file storage that varies by staff member.

Manual assembly across 10–20 properties typically takes two to four weeks and still produces gaps: accounts that changed mid-period (new vendor, new meter number, new account number), properties acquired during the hold where prior-owner records were never transferred, and invoices paid via ACH without retaining the original document.

What documentation gaps look like to a buyer is not "this operator lost some files." It looks like "this operator does not have a handle on their utility expenses." That narrative supports a price reduction or an escrow request independent of whether the gaps reflect any actual billing problem.

Normalizing the Expense Run Rate

Raw trailing-12-month utility expense is rarely the right underwriting figure. Three types of distortion require adjustment before the number represents the forward run rate.

Consumption anomalies: invoices in the trailing period that reflected abnormal usage (a confirmed leak, an equipment failure, an estimated read that was later trued up) inflate the baseline. Each anomaly should be identified, quantified, and presented alongside the raw actuals with the adjustment explained and supported by the invoice and consumption data.

Rate schedule normalization: if a rate increase took effect mid-year, the trailing 12-month average understates the forward run rate. The correct underwriting figure is the current rate schedule applied to normalized consumption, not the blended average of the last 12 months at mixed rates.

Occupancy normalization: for master-metered properties with significant occupancy variance during the trailing period, the raw total reflects a mix of occupancy levels that may not represent stabilized operations. The normalized figure adjusts to a stabilized occupancy assumption and presents the trailing data alongside the adjustment methodology.

This analysis requires consumption-level data, not just invoice totals. An operator who can only show total dollars paid per month cannot distinguish a consumption anomaly from a rate error from a billing period change. The consumption figures in the invoice history are what make the normalization defensible to a buyer or lender who reviews it.

Confirming Payment History and Open Items

Alongside the invoice record, the diligence package needs to confirm the payment side: that every invoice in the period was paid, that no accounts carry an unpaid balance, and that no active billing disputes exist. Lenders treat an account in arrears or a dispute running for six months as a management gap, regardless of the dollar amount.

This step also requires a coverage audit: confirm that every utility account for every property has a continuous record for the full trailing period. Accounts that were closed and reopened, renamed, or transferred to a new account number during the period are common gaps. Each one needs documentation of continuity of coverage: the physical service was continuous even if the account structure changed.

Forward Rate Schedule Review

Buyers underwriting an acquisition want to know whether the normalized trailing expense is a reliable guide to the forward run rate. A material rate increase scheduled to take effect in the next 12 months changes the answer. Buyers will discover scheduled rate changes whether the seller discloses them or not.

The disclosure approach: include the current rate schedule for each major utility vendor in the diligence package, note any rate changes effective within the next 12 months, and show the impact on the forward expense at normalized consumption. Sellers who provide this analysis with supporting documentation control the framing; sellers who don't invite the buyer to make their own, typically conservative, assumptions.

Vacant Cost Recovery History

For operators running a Vacant Cost Recovery program, the recovery track record is a positive disclosure that supports NOI. The VCR history should show total recoveries by property and period, the methodology used, and the platform managing the program. This demonstrates active management of a line item that most operators leave untracked, and it makes the recovery component of NOI verifiable rather than assumed.

Buyers who can trace VCR income to documented recovery records (invoices received, reviewed, and credited per a defined program) apply a lower risk discount to that income stream than to VCR income that appears in the operating statement without supporting data. A documented program produces a more defensible number at the time it matters most.

The Preparation Timeline

The document assembly problem becomes a deal-timeline problem when it starts after the LOI. At that point, the buyer's diligence clock is running and the seller is assembling records in parallel with legal, title, and financing, all of which are also time-sensitive.

At 90–120 days before target close: identify all active utility accounts by property, confirm no unpaid balances or active billing disputes, and begin pulling invoice history from vendor portals. Run the coverage audit to confirm that every property and every utility type has a continuous record for the trailing 24–36 months.

At 60 days: the organized invoice record should be complete. Run the normalization analysis: identify anomalies in the trailing period, quantify them, and prepare the normalized expense summary with supporting invoice and consumption data.

At 30 days: the full utility expense package (organized invoice records, normalization analysis, forward rate schedule review, payment confirmation, and VCR recovery history if applicable) should be ready to load into the data room on day one. Buyers who receive a complete, organized utility package at data room open close faster. Delays give buyers more time to find issues and give lenders more time to add conditions.

How Billee Supports Utility Diligence

Billee's platform centralizes every processed invoice by property, vendor, and billing period from enrollment forward. Every invoice processed through app.billee.ai is retained and accessible by period, property, and utility type without a manual assembly project. For an operator with 18 months of Billee enrollment, a buyer's 24-month request means 18 months from Billee and 6 months to source from prior records; that is a manageable gap rather than a full assembly project.

The exception reporting Billee provides during normal AP operations doubles as normalization support. The operator can show which invoices were flagged as anomalous during the audit step, what the issue was, and how it was resolved before payment. That documentation makes the normalization analysis defensible: it is the documented output of an independent audit running in real time throughout the hold, not a retroactive characterization assembled for the data room.

For operators who want to understand how Billee builds the record that diligence requires, the CFO utility reporting article covers the five reporting components that support portfolio-level visibility, and the utility vendor management overview explains how invoice data is captured and retained from enrollment forward.

Implementation takes 45 days. Vendor onboarding, rate schedule configuration, and PMS integration are handled by the Billee team.

Billee maintains the utility cost documentation that refinancing and disposition require as a standard output of normal AP processing, with no assembly project at close. See how it works for your portfolio.

FAQ: Preparing Utility Cost Data for Refinancing or Disposition

What utility documentation do lenders require for multifamily refinancing?

Lenders underwriting multifamily loans, including Fannie Mae and Freddie Mac agency programs, require 12–24 months of utility expense history as part of operating expense verification. This includes invoice records by property and utility type, confirmation of no unpaid balances, and no unresolved billing disputes with active vendors. Gaps in coverage or missing invoice copies can trigger reserve requirements or extend the underwriting timeline.

What utility data do buyers review in a multifamily acquisition?

Buyers in a multifamily acquisition typically request 24–36 months of utility invoice history by property, organized by vendor and utility type. They are looking to verify that the seller's stated NOI is supportable, that the trailing expense represents the forward run rate, and that any anomalies in the period have been identified and normalized. Undisclosed anomalies become negotiating leverage; disclosed anomalies with supporting documentation do not.

How do I normalize utility expense for lender or buyer underwriting?

Normalizing utility expense requires three adjustments: removing consumption anomalies from the baseline (leaks, equipment failures, estimated reads), recalculating at the current rate schedule if rates changed mid-year, and adjusting for occupancy if the trailing period had significant vacancy variance. Each adjustment should be supported by the underlying invoice and consumption data. Normalization requires consumption-level data, not just invoice totals; total dollars paid per month cannot distinguish an anomaly from a rate change.

What happens if utility records are incomplete or missing during due diligence?

Documentation gaps in a utility diligence package give buyers a negotiating lever regardless of whether the gaps reflect actual billing problems. Buyers interpret missing or disorganized records as a management gap, which supports requests for price adjustments or escrow holds. Lenders may require a utility expense reserve when the operating expense history cannot be fully documented. The cost of organizing utility records in advance consistently exceeds the cost of a price concession at close.

When should I start preparing utility cost data before a sale or refinancing?

Start 90–120 days before the target close date. At 90 days: identify all active utility accounts and run a coverage audit to confirm continuous records for the trailing 24–36 months. At 60 days: complete the invoice record assembly and run the normalization analysis. At 30 days: the full diligence package (records, normalization, forward rate review, VCR history) should be ready to load into the data room on day one. Starting after the LOI is signed puts the assembly on the critical path of the transaction timeline.

Sources

Fannie Mae, "Multifamily Selling and Servicing Guide," accessed June 2026. (Operating expense documentation requirements for agency loan underwriting.)

National Apartment Association, "Income & Expense Survey," accessed June 2026. (Utility expense as a percentage of total multifamily operating expenses by property type.)

Zego, "The Top 3 Utility Accounts Payable Mistakes Multifamily Companies Make," 2025. (Cites ENGIE Impact audit finding: at least 17% of utility invoices contain a billing error.)

Insights and Industry Trends