How to Prepare a Billing Methodology Audit for Multifamily Properties

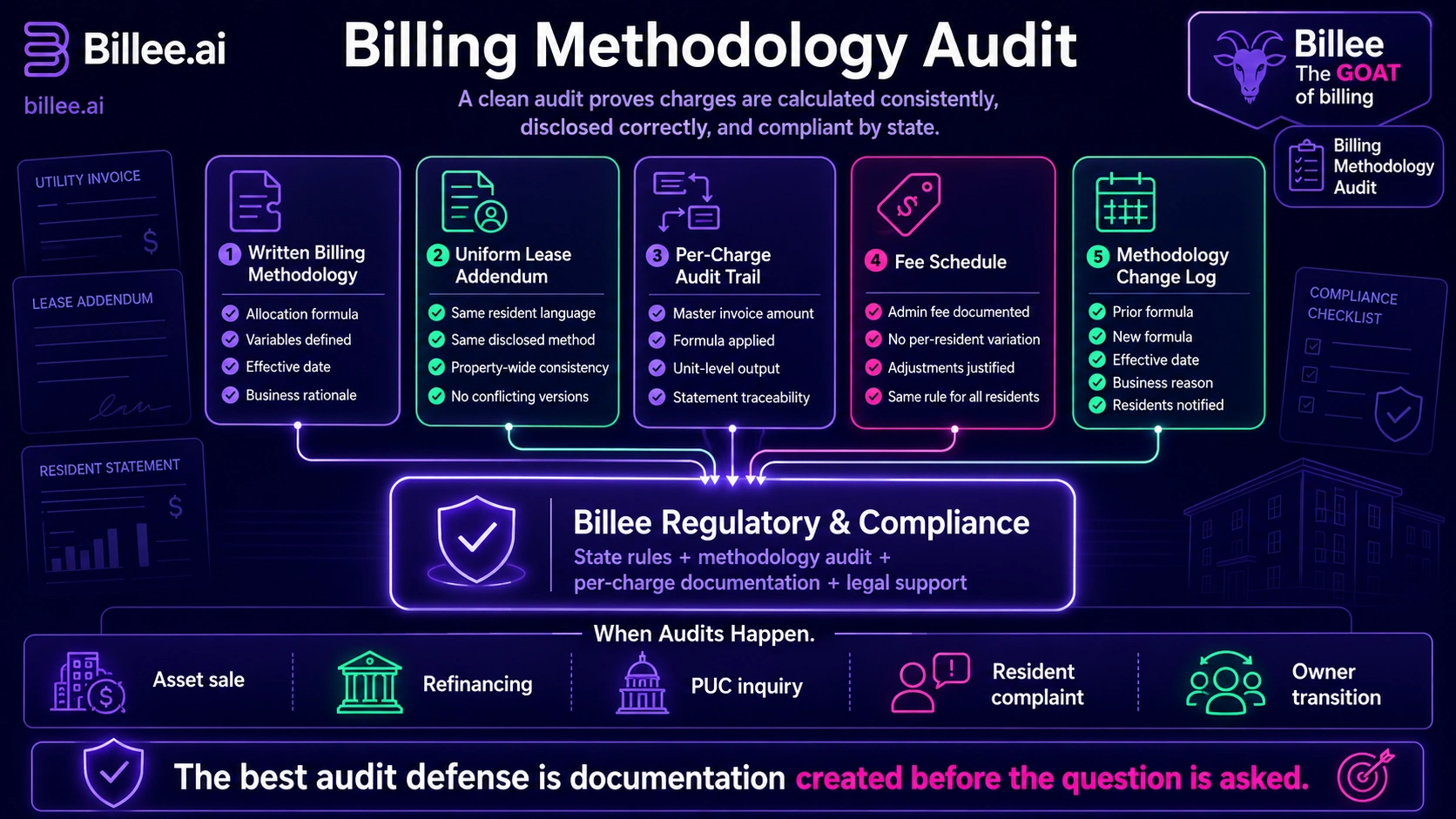

A billing methodology audit reviews whether utility charges are calculated consistently, disclosed correctly, and compliant with state regulations at each property in a portfolio. The audit is most commonly triggered by an asset sale, refinancing, PUC inquiry, or resident complaint, but it also functions as a recovery tool: a 2026 review of 650 multifamily properties found 148 meter accounts on incorrect rate structures across 136 properties, representing $1.85 million in projected annual savings. Preparing for one requires five documents: a written billing methodology, uniform lease addenda, a per-charge audit trail, a fee schedule, and a change log. Billee's Regulatory & Compliance service audits each property's methodology against state PUC rules and provides access to legal support to remediate gaps before they become findings.

Key Takeaways

A billing methodology audit is both a compliance exercise and a recovery tool. Incorrect rate structures, not just formula errors, are among the most common findings and they compound silently across every billing cycle.

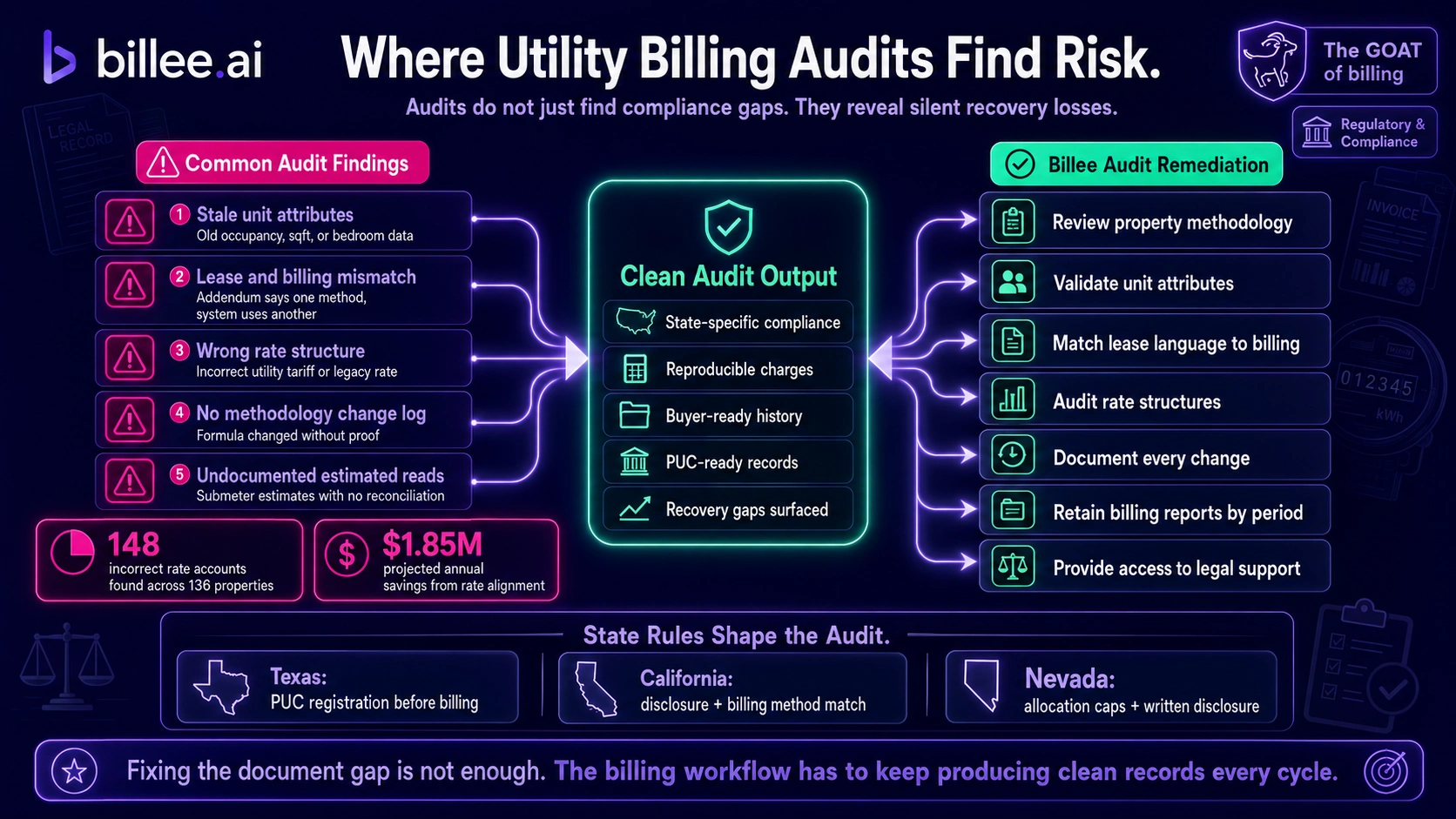

A 2026 review of 650 multifamily properties found that 148 meter accounts across 136 properties were on incorrect or suboptimal rate structures, representing $1.85 million in projected annual savings from rate alignment alone.

The five documents that determine audit outcomes: a written billing methodology, a lease addendum applied uniformly to all residents, a per-charge audit trail, a fee schedule with no per-resident variation, and a methodology change log.

Texas operators must register their billing methodology with the Texas PUC under 16 TAC Chapter 24 before billing residents for allocated utility service. Registration is a precondition for a clean audit, not an output of one.

Asset sale and refinancing audits carry different stakes than routine reviews. Due diligence buyers typically request 24 months of utility billing history, and gaps in that record slow closings and can affect valuations.

An audit finding is only as durable as the workflow behind it. Fixing documentation gaps without fixing the underlying billing process produces the same findings at the next audit.

What a Billing Methodology Audit Actually Reviews

A billing methodology audit covers four distinct layers of a property's utility billing operation.

The written methodology document. An audit starts by confirming that a written record exists for each property: the allocation formula used (occupant-based, square-footage-based, or hybrid for RUBS; meter readings and rate schedule for submetering), the effective date, and the business rationale. Without this document, no other record can prove the billing was consistent.

The allocation formula and unit attributes. A correct formula produces incorrect charges when fed stale data. An audit checks whether the occupant counts, square footage figures, or bedroom counts used in the RUBS denominator match the actual resident population in each billing period. Outdated unit attributes are the single most common finding in billing methodology audits.

The lease addendum language. The addendum signed by residents must describe the same methodology actually used to generate charges. A property where lease addenda reference an "occupant-based RUBS formula" while the billing system runs on square footage creates a factual conflict that is difficult to defend in a complaint or regulatory inquiry.

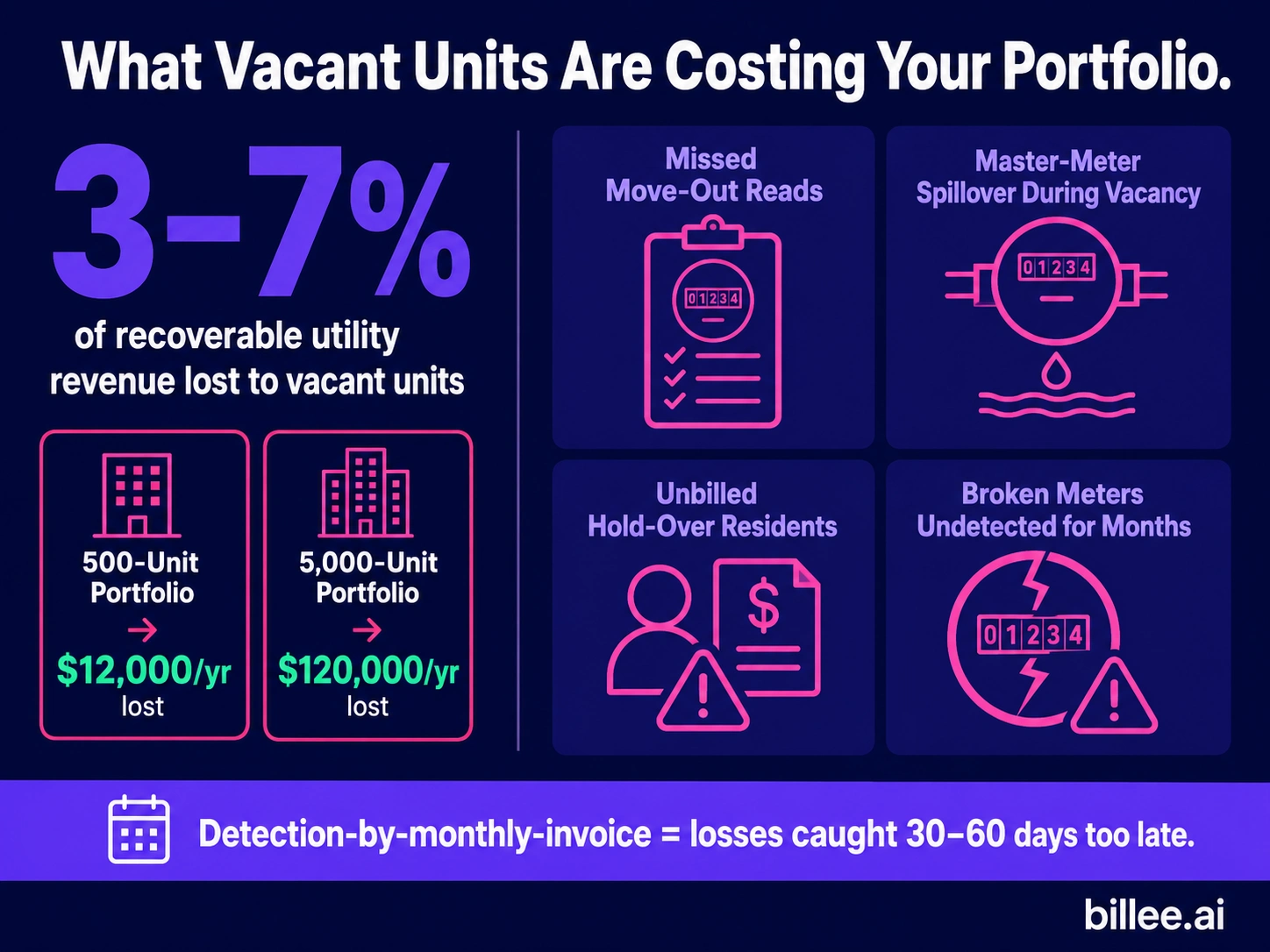

The rate structure. This layer is most often overlooked. A property can run a correct RUBS formula and still be on the wrong utility rate, paying general commercial rates instead of multifamily-specific ones, or remaining on a legacy rate tier that no longer matches actual usage. Utilities account for 15%–20% of total multifamily operating costs, and a misaligned rate structure inflates or suppresses that figure silently.

Five Triggers That Require a Billing Methodology Audit

Asset sale or acquisition. Buyers in multifamily due diligence typically request 24 months of utility billing history. They are looking for documentation that charges were consistent, correctly allocated, and applied uniformly. Gaps in this record slow closings. Systematic under-billing discovered during due diligence understates the property's actual NOI recovery potential; systematic over-billing creates liability the seller must account for.

Refinancing. Lenders want confidence that the NOI figure they are underwriting reflects real, sustainable recovery, not a period of inadvertent over-billing or favorable occupancy assumptions. A per-charge audit trail connecting each cycle's charges to verified utility invoice amounts supports the lender's own underwriting review.

PUC inquiry or resident complaint. Regulatory inquiries from a state Public Utility Commission move quickly and require documentation created at the time of the billing decision, not reconstructed afterward. Resident complaints that escalate to the state level typically trigger a request for the written methodology and proof that it was disclosed to the resident before the first charge.

Owner or operator transition. A property that changes ownership or management company needs a billing handoff that documents the methodology in place, the vendor accounts and credentials, and the per-charge records from prior periods. Transitions that skip this step leave the incoming operator billing under a methodology they cannot document.

First-time RUBS or submetering setup. In Texas, operators must register allocated utility billing with the Texas PUC before sending the first resident bill. The written methodology and disclosure language must be in place before the first billing cycle. Skipping this step makes every subsequent bill a potential violation.

The Five Documents That Determine Your Audit Outcome

Written billing methodology. One document per property, stating the formula, the variables, the effective date, and the business rationale. This document must be updated every time the methodology changes. Without it, there is no baseline against which to measure consistency.

Uniform lease addendum. Every resident at the property must have signed the same addendum language describing the same billing methodology. A property where some residents signed one version and others signed a different version has a documentary record of inconsistency before the first bill was ever sent.

Per-charge audit trail. For every billing cycle, a record showing how each resident's charge was derived from the master utility invoice: total cost, allocation formula applied, and per-unit output. For submetered properties, this includes meter readings, consumption units, and the rate applied. This is the document that proves, in a complaint or audit, that every resident's charge was produced by the same process.

Fee schedule with no per-resident variation. A record showing the administrative fee charged each cycle, with documentation confirming the same fee was applied to every resident. Any fee adjustment made for a documented business reason must be applied consistently to all residents in the same situation.

Methodology change log. Every change to the billing methodology must be recorded: the prior formula, the new formula, the effective date, the business reason, the residents notified, and the notification date. A mid-lease methodology change applied without uniform, documented notice to all affected residents is one of the most direct paths to a regulatory complaint.

The Most Common Gaps Auditors Find

Stale unit attributes. The RUBS formula is correct, but it is running on occupant counts or square footage data that was not updated after unit mix changes, lease-ups following a renovation, or shifts in occupancy assumptions. The formula produces the wrong number for every resident in every cycle until the inputs are corrected. This finding is common precisely because it is invisible without an audit: the system is doing exactly what it is configured to do.

Lease and billing mismatch. The lease addendum describes one methodology, and the billing system is running another. This happens most often when a property transitions from RUBS to submetering, or vice versa, without updating the lease language for all affected residents. The mismatch creates a factual conflict that an auditor, a regulator, or a buyer's counsel will surface.

Wrong rate structure. Rate structures are highly localized, frequently updated by utilities, and rarely reviewed automatically. Properties that have undergone renovation, ownership transitions, or significant occupancy shifts since the rate was last evaluated are most likely to have a structural misalignment. Because utilities account for a substantial share of operating costs, even a one-to-two percent rate misalignment has a measurable impact on net operating income.

No methodology change log. Many operators change their billing methodology without creating a contemporaneous record of the change, the reason, and the residents notified. When an audit, a complaint, or a due diligence request asks for evidence the change was handled correctly, no log means no defense.

Estimated reads without documentation. Submetered properties that record estimated reads during equipment downtime or restricted access must document when the estimate was used, what it was based on, and how the subsequent actual read reconciled it. Undocumented estimated reads are routinely flagged in submetering audits.

State Rules That Define What a Clean Audit Looks Like

What counts as a compliant billing methodology varies by state. A portfolio operating across multiple states must pass a different compliance standard in each jurisdiction.

Texas is the most prescriptive state for multifamily utility billing. Under 16 TAC Chapter 24 (Subchapter I), operators must register allocated utility billing with the Texas PUC before the first bill, make the underlying utility invoices and calculation data available to residents on request, and maintain submeter testing records for the life of the equipment. A clean Texas audit requires proof of PUC registration, not just documentation of the formula.

California governs submetering under Civil Code §1940.9, which requires specific lease disclosure language before submetering begins. CPUC General Order 103-A adds requirements for billing practices at master-metered properties. A California audit focuses on whether the disclosure was made correctly and whether the billing practice matches the disclosed method.

Nevada sets limits on RUBS allocation percentages under NAC Chapter 392 and requires written disclosure of the billing method before occupancy. An audit in Nevada checks the allocation cap and the timing of the disclosure relative to the first billing cycle.

States without specific PUC submetering or RUBS regulations still apply general landlord-tenant law and, where applicable, HUD utility allowance rules for voucher-assisted properties. As covered in Billee's fair housing billing guide, the Fair Housing Act's non-discrimination requirement applies to utility billing regardless of state-level PUC rules, and billing consistency documentation serves both regulatory and fair housing defense simultaneously.

How Billee Prepares Your Portfolio for a Billing Methodology Audit

Billee's Regulatory & Compliance service audits each property's billing methodology against the state-specific PUC rules applicable to that property's jurisdiction. The audit surfaces gaps in the written methodology, the lease disclosure, and the per-charge record. Billee's team provides access to legal support to remediate findings before they appear in a regulatory inquiry or a buyer's due diligence review.

The billing records generated each cycle, including the locked billing reports produced by the Billee platform, are retained and organized by property and period. When an audit, a refinancing package, or a sale process requires 24 months of billing history, that documentation is retrievable without a reconstruction effort.

Implementation takes 45 days. Vendor onboarding, state-specific billing configuration, and PMS integration are handled by the Billee team.

Billee audits billing methodology, documents the per-charge audit trail, and provides access to legal support for multifamily portfolios preparing for an audit, a sale, or a regulatory inquiry. Talk to the team.

FAQ: Billing Methodology Audits for Multifamily Properties

What does a billing methodology audit cover?

A billing methodology audit reviews four areas of a property's utility billing operation: the written methodology document, the allocation formula and the unit attributes feeding it, the lease addendum language, and the rate structure applied by the utility. A complete audit confirms that all four are internally consistent, compliant with applicable state regulations, and supported by contemporaneous documentation created at the time of each billing decision.

When should a multifamily operator schedule a billing methodology audit?

Five triggers most commonly require a billing methodology audit: preparation for an asset sale or acquisition, refinancing (where lenders require a verifiable NOI figure), a PUC inquiry or resident complaint, an owner or operator transition, and first-time RUBS or submetering setup. In Texas, the billing methodology must be registered with the Texas PUC before the first resident bill, which means the audit is a prerequisite for billing, not a review after the fact.

What is the most common finding in a utility billing audit?

The most common finding is stale unit attributes feeding an otherwise correct RUBS formula. Occupant counts or square footage data that were not updated after a lease-up, renovation, or occupancy change produce systematic over- or under-billing across every resident in every subsequent cycle. The error is invisible without an audit because the billing system is doing exactly what it is configured to do.

Does Texas require billing methodology registration before billing residents?

Yes. Under 16 TAC Chapter 24, Texas operators must register allocated utility billing with the Texas PUC before sending the first resident bill. The registration requires a written statement of the allocation methodology and disclosure of the underlying utility rate information. Billing residents before completing registration makes each bill a potential regulatory violation under the Texas Utilities Code.

How does a billing methodology audit affect a property's value at sale?

Due diligence buyers in multifamily acquisitions typically request 24 months of utility billing history. A portfolio with a documented, consistent methodology and a clean per-charge audit trail supports the seller's NOI figures and removes a potential point of valuation dispute. Gaps in the billing record, systematic over-billing, or compliance deficiencies discovered during due diligence can slow the closing process and, in some cases, affect pricing.

Sources

Conservice, "What 650 Property Audits Revealed About Utility Rate Misalignment," March 30, 2026.

Texas Public Utility Commission, "Tenant Guide: Allocated Utility Service," accessed July 2026.

Texas Public Utility Commission, "Registration of Submetered or Allocated Utility Service," accessed July 2026.

Multifamily.loans, "Multifamily Utility Considerations for Investors," accessed July 2026.

Think Utility Services, "Mastering Utility Billing Compliance: A Guide for Multifamily Operators," July 2025.

Insights and Industry Trends