Utility Billing Compliance for Affordable Housing: LIHTC and Section 8 Rules Explained

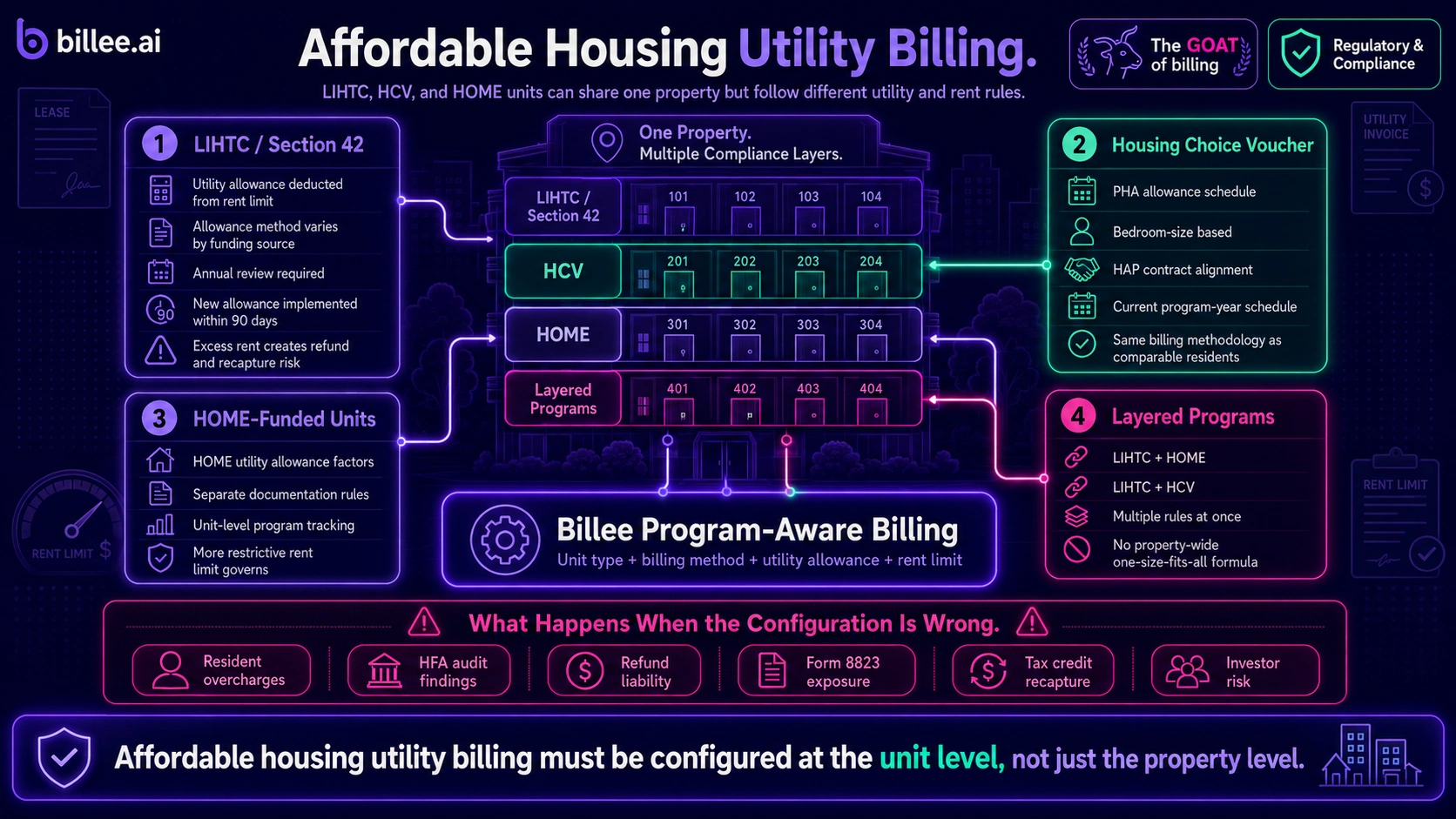

Affordable housing utility billing operates under a compliance framework that does not exist in conventional multifamily. LIHTC properties under Section 42, Housing Choice Voucher properties, and HOME-funded buildings each have distinct rules governing how utility costs are treated in gross rent calculations, which billing methods are permitted, and how frequently allowances must be updated. Getting any part of this wrong risks tax credit recapture, HFA audit findings, and resident overcharges that must be refunded. Billee's Regulatory & Compliance product and Billing & Recovery Engine are configured for affordable housing program layers at implementation, so the billing methodology matches the funding structure from day one.

Key compliance requirements at a glance:

- LIHTC properties must deduct an applicable utility allowance from gross rent; the calculation method is determined by building type and funding source under Treas. Reg. §1.42-10(b)

- Updated utility allowances must be implemented within 90 days of the effective date under 26 CFR §1.42-10(c); this deadline is the single most common LIHTC compliance finding in HFA audits

- RUBS charges count toward gross rent in LIHTC properties; submetered actual-consumption charges do not (per the 2016 IRS final rule); this distinction has significant rent-limit implications

- HCV / Section 8 properties must use PHA utility allowance schedules tied to bedroom size for the applicable program year

- Layered programs (LIHTC + HOME, LIHTC + HCV) must satisfy both sets of rules simultaneously; the more restrictive rent limit always governs

- FY 2026 HUD Multifamily Utility Allowance Factors became effective February 11, 2026; properties using the HUD model must have updated by May 12, 2026

The Compliance Framework for Affordable Housing Utility Billing

LIHTC / Section 42 Properties

Under IRC Section 42, gross rent includes both what the resident pays as rent and any utility costs the resident pays directly. The maximum allowable gross rent equals the applicable LIHTC rent limit minus the applicable utility allowance. Four methods exist for determining the utility allowance under Treas. Reg. §1.42-10(b), and the applicable method depends on whether the building receives Rural Housing Service (RHS) assistance, has residents receiving HUD tenant assistance, or falls into neither category (in which case the local PHA schedule applies).

Operators must know which category each building falls into. A mixed-development portfolio may use different methods for different buildings.

Section 8 / Housing Choice Voucher Properties

HAP contracts specify which utilities are owner-paid and which are resident-paid. PHAs maintain their own utility allowance schedules under 24 CFR Part 982, updated periodically, and the allowance for each unit is tied to bedroom size. If a PHA updates its schedule and the property does not reflect the new allowance in its rent calculation, the property may be collecting more than the program permits.

HUD's proposed 2026 budget cuts create uncertainty around program staffing, but the regulatory requirements on operators do not change.

HOME Program Properties

HOME-funded units require a utility allowance deduction similar to LIHTC, using HUD-published HOME utility allowance factors. Layered developments, the most common structure for affordable housing built after 2000, combine LIHTC with HOME, HCV, or both. In those cases, every rent-restricted unit must satisfy both programs simultaneously, and the more restrictive rent limit governs.

Operators running mixed-program portfolios need billing configurations that track which program type governs each unit, not a single formula applied to all residents.

RUBS vs. Submetering: The Compliance Difference in Affordable Housing

| RUBS | Submetering | Owner-Paid | |

|---|---|---|---|

| Counts toward gross rent (LIHTC)? | Yes | No (per Treas. Reg. §1.42-10(e)) | N/A — resident not billed |

| Rent limit risk | High if utility rates rise | None | None |

| Billing cap | Rent limit minus utility allowance | Utility company's direct rate | No resident charge |

| Utility allowance deduction required? | Yes | Yes | Yes |

| Administrative complexity | Moderate | Low (LIHTC-clean) | Low |

| Who absorbs cost overruns | Operator if gross rent ceiling hit | Operator if above utility rate cap | Operator always |

| Most common in large portfolios? | Rarely | Yes | Yes |

Why RUBS Creates Compliance Risk in LIHTC Properties

RUBS charges are treated as tenant-paid utilities under IRS rules for LIHTC properties, which means they count toward gross rent. The practical consequence: a LIHTC property running RUBS must ensure that the allocated RUBS charge plus the resident's base rent never exceeds the applicable rent limit minus the utility allowance. As utility costs rise, this ceiling becomes binding.

Operators who set up RUBS without modeling the gross rent impact can inadvertently push residents above the rent cap in high-utility months, creating a retroactive compliance problem.

How Submetering Changes the Calculation

The 2016 IRS final rule, codified at Treas. Reg. §1.42-10(e), established that utility costs paid by a resident based on actual submetered consumption are treated as paid directly to the utility company; they do not count toward gross rent. This gives affordable housing operators substantially more billing flexibility: submetered charges can be billed above what RUBS would have allowed, without affecting program compliance, provided charges do not exceed what the utility company would have charged directly.

For renewable energy sources, the same rate cap applies.

Which Method Fits Which Property Type

Submetering is more administratively clean for LIHTC compliance because it removes utility costs from the gross rent calculation entirely. RUBS remains viable where total charges plus rent stay comfortably under the rent limit, but operators need to model this for each unit type and review it whenever utility rates change.

A third option, owner-paid utilities with one inclusive rent, eliminates billing compliance risk altogether but leaves the operator absorbing all utility costs. Most large affordable housing portfolios use submetering or owner-paid utilities rather than RUBS precisely because of the gross rent complexity.

The Utility Allowance Update Process

Five Methods for Calculating Utility Allowances

Under Treas. Reg. §1.42-10, five calculation methods are available for properties not receiving RHS or HUD assistance. These are: (1) the HUD Utility Schedule Model using form HUD-52667, with utility rates no more than 60 days old at the time of calculation; (2) HUD Multifamily Utility Allowance Factors, published annually (FY 2026 factors effective February 11, 2026); (3) an energy consumption model based on actual building characteristics and local utility rates; (4) a utility company estimate from the specific supplier serving the property; and (5) the applicable PHA utility allowance schedule.

Each method produces a different result. Properties can select any eligible method but must apply it consistently and document the selection.

The 90-Day Implementation Rule

Under 26 CFR §1.42-10(c), when the applicable utility allowance changes, the new allowance must be used to calculate gross rents no later than 90 days after the change becomes effective. This is not a soft deadline; missing it is a compliance event. For properties using HUD Utility Allowance Factors, the 90-day clock started on the February 11, 2026 effective date, meaning updated allowances had to be in use by May 12, 2026.

Properties using PHA schedules must track when their local PHA publishes updated tables and start the same 90-day clock on that date.

Documentation Requirements for HFA and IRS Review

Operators must retain a copy of the document establishing the utility allowance for each year, including the method used, the effective date, and the source data. For properties using the HUD Utility Schedule Model, the utility rate data must be dated no more than 60 days before the calculation and must be retained.

HFA physical inspections increasingly cross-reference utility billing records against allowance documentation. An operator who can produce a monthly bill but not the supporting allowance calculation is generating an audit finding even if the math was correct.

Common Compliance Failures and What They Cost

Stale Utility Allowances

Using an allowance that has not been updated within 12 months, or that has not been updated within 90 days of an applicable change, is a violation. It is also the most frequently cited utility billing finding in HFA audits, because energy prices move while allowances sit static. An underestimated allowance means residents are being charged too much relative to the rent limit; an overestimated allowance means the operator is collecting less rent than permitted but residents are not overcharged. Both are findings; only the former creates refund liability.

RUBS Misclassification

Treating RUBS charges as equivalent to submetering for gross rent purposes is a structural error that can put an entire portfolio out of compliance simultaneously. Operators who converted from submetering to RUBS, or who added RUBS for utility types not previously billed, without reassessing the gross rent impact may be in violation across every affected unit. Billee's billing audit process identifies this pattern during implementation.

Layered Program Misalignment

Properties combining LIHTC with HOME or HCV frequently run into unit-level misalignment, where the billing system applies one program's rent limit to a unit governed by another. This occurs most often when the PMS tracks program type at the property level rather than the unit level, and the billing configuration inherits that error. The consequence is systematic overcharges to the most income-restricted residents, which require retroactive correction and disclosure to the state HFA.

Refund and Recapture Exposure

Excess rent collected from rent-restricted residents must be refunded. If the overcharge is found during an IRS audit or state HFA inspection, the operator may also face tax credit recapture; investors can lose some or all of their credits for the affected years. The audit lookback period for LIHTC compliance is typically the extended use period (15–30 years depending on agreement terms), meaning errors from years ago can surface in a current review.

State Rules That Affect Affordable Housing Utility Billing

State HFA Requirements on Top of Federal Rules

State housing finance agencies administer the LIHTC program at the state level and can impose requirements stricter than the federal baseline. Some states require specific utility allowance calculation methods, more frequent updates, or additional documentation. Colorado's HB26-1013 (signed March 2026) requires direct metering or submetering for new residential buildings permitted after July 1, 2027; this applies to affordable housing new construction in Colorado and affects how developers configure utility billing infrastructure before permitting.

PUC Registration for Submetered Affordable Properties

Texas requires operators using submetering for allocated utility billing to register with the Texas Public Utility Commission under 16 TAC Chapter 24 before sending the first resident bill. This requirement applies to affordable housing properties the same as conventional multifamily. An unregistered affordable housing operator in Texas is simultaneously violating state utility regulations and potentially misconfiguring the gross rent calculation, a compound compliance exposure.

California's CPUC General Order 103-A imposes billing practice requirements on master-metered properties, including affordable housing.

How Billee Handles Affordable Housing Utility Billing

Program-Aware Billing Configuration

Billee's Billing & Recovery Engine is configured at the unit level at implementation, distinguishing LIHTC units, HCV-assisted units, and HOME-funded units within the same property. The billing methodology (RUBS, submetering, or owner-paid) is matched to what is permissible under each program layer, and the utility allowance in effect for each unit type is built into the gross rent calculation rather than applied as a manual adjustment.

Utility Allowance Tracking and Annual Review Support

Billee flags when a utility allowance is approaching its annual review requirement and when HUD publishes updated Utility Allowance Factors. The 90-day implementation clock is tracked by the Billee account team, not by the property manager relying on calendar reminders. PMS integration with Yardi, RealPage, and Entrata keeps unit-level program type and resident data current, so bedroom-size-specific allowances reflect actual occupancy.

Audit-Ready Documentation Per Unit

Every billing cycle generates a per-unit record that includes the utility allowance applied, the billing method, the applicable rent limit, and the resulting gross rent. This documentation is available for HFA and IRS review on demand. Implementation takes 45 days; vendor onboarding, state-specific configuration, and PMS integration are handled by the Billee team.

FAQ: Affordable Housing Utility Billing Compliance

What is a utility allowance in affordable housing? A utility allowance is a dollar amount representing the estimated monthly cost of resident-paid utilities in a unit of a given size and type. In LIHTC and HOME properties, the utility allowance is subtracted from the applicable rent limit to determine the maximum rent the operator can charge. It is not optional; properties must calculate and apply it correctly every year.

Does LIHTC allow RUBS billing? Yes, RUBS is permitted in LIHTC properties, but the RUBS charge counts toward gross rent. The resident's base rent plus the RUBS allocation must not exceed the applicable rent limit minus the utility allowance. This constraint becomes binding as utility rates rise, and operators must model it at the unit level before implementing RUBS.

Do submetered charges count toward gross rent in LIHTC? No. Under the 2016 IRS final rule codified at Treas. Reg. §1.42-10(e), charges based on actual submetered consumption are treated as paid directly to the utility company and excluded from gross rent, provided they do not exceed the utility company's direct rate. This is the primary compliance advantage of submetering over RUBS in affordable housing.

How often must I update my utility allowance? At least annually for LIHTC properties. Additionally, any time the applicable utility allowance changes (for example, when HUD publishes new Utility Allowance Factors or a PHA updates its schedule), the new allowance must be implemented within 90 days of the effective date per 26 CFR §1.42-10(c).

What happens if my utility allowance is out of date? An out-of-date allowance is a compliance event. If the stale allowance underestimates actual utility costs, residents may be charged rent that exceeds the program's gross rent limit, creating refund liability. If it overestimates costs, the operator is collecting below-market rent but residents are not harmed. State HFAs cite stale allowances in physical inspections and file them as Form 8823 violations with the IRS.

What is the penalty for excess rent in a LIHTC property? Excess rent must be refunded to affected residents. If found in an IRS or HFA audit, the property owner may face tax credit recapture; investors can lose credits for the year of the violation and, in severe cases, earlier years as well. The extended use period (15–30 years) means past billing errors remain audit-eligible for a long time.

Do HOME and LIHTC have the same utility allowance rules? No, though they are similar. HOME uses HUD-published HOME utility allowance factors rather than the five LIHTC methods. In layered LIHTC/HOME properties, both sets of rules apply simultaneously, and the more restrictive rent limit governs each unit. The documentation requirements also differ; operators must satisfy both programs' audit trail requirements.

Does Texas require PUC registration for submetered affordable housing properties? Yes. Texas 16 TAC Chapter 24 requires all master-metered properties using submetering or allocated billing to register with the Texas Public Utility Commission before issuing the first resident bill. This applies to affordable housing properties on the same terms as conventional multifamily. Operating without registration is a violation of state utility rules, independent of the property's LIHTC or HCV compliance status.

Billee configures billing methodology and utility allowance tracking at the unit level for affordable housing portfolios, with audit-ready documentation built into every billing cycle. Talk to the team.

Sources

- Cornell Legal Information Institute, "26 CFR §1.42-10 — Utility Allowances," accessed July 2026.

- Novogradac, "Determining Applicable Utility Allowances for LIHTC Properties," accessed July 2026.

- Illinois Housing Development Authority, "LIHTC & HOME Compliance Manual," April 2026.

- Federal Register, "Utility Allowances Submetering — Final Rule," March 3, 2016.

- HUD User, "HUD Multifamily Utility Allowance Factors," FY 2026 (effective February 11, 2026).

- Novogradac, "Master Meters, Applicable Rates, Actual Use: LIHTC Utility Allowance," accessed July 2026.

- Holland & Knight, "Existing Colorado Multifamily Housing Developments Can Continue," April 2026.

- Electronic Code of Federal Regulations, "24 CFR Part 982 — Housing Choice Voucher Program," accessed July 2026.

Insights and Industry Trends

Explore more insights